With private home prices at a high in 2023, a common question is why anyone still bothers to upgrade. With new launch condos priced at well over $2,000 psf, and resale condos also rising, it begs the question: wouldn’t we be better off sticking to our flat, and investing the money elsewhere? While some single-digit millionaires may think so, the majority still prefer making the leap to private homes. Here’s why:

The current private home market in 2023

Property isn’t something that we can generalise well, because there are so many differences between homes. However, we will look at overall price movements (in an admittedly crude way) to get a snapshot of the market as it stands in 2023.

Based on data from Square Foot Research, we can see that new none-landed home prices currently average $2,688 psf, up by around 110.8 per cent from the last decade:

Even if we look at the slower paced resale condo market, we can see prices now average $1,544 psf. Still an increase of around 24 per cent from the last decade.

The private landed market has seen the most significant price increase over the past decade, and is currently at $1,774 psf. This is up around 44 per cent from the previous decade.

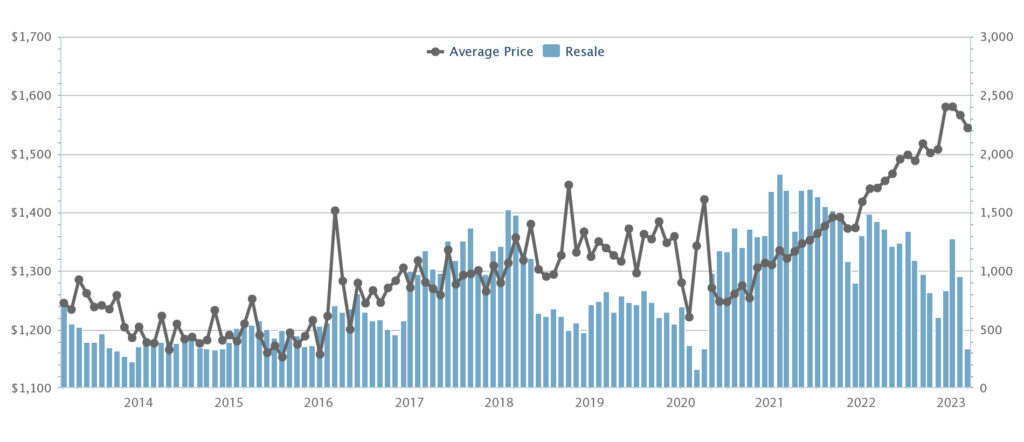

HDB resale prices – which often determine whether one has the means to upgrade to private property – have surged in the post-Covid period. But if we look at HDB prices over the same period, we can see that, on average, resale flats have failed to keep pace with the private non-landed market (be it resale or new):

With this is mind, we can begin to grasp the rationalisations of some single-digit millionaires, who are still eager to sell their flats and upgrade.

Why upgrade even when private home prices are high?

- FOMO effect, as the price gap is visibly widening

- Private property ownership is still seen as a safety net

- Legacy planning issues

- Cash-Out Refinancing options for private homes

1. FOMO effect, as the price gap is visibly widening

Fear Of Missing Out (FOMO) kicks in during property bull markets like 2023. It’s a constant worry that if you don’t upgrade now, you won’t be able to afford it later. This fear is accentuated by historical precedent, in which each property bull market has seen prices pushed higher than the last (the last property peak was in 2013).

Even if there’s no fear of eventual affordability, there are issues regarding cashflow and the initial cash outlay:

For private properties, the minimum down payment is currently 25 per cent (five per cent in cash, and another 20 per cent in CPF). This assumes you qualify for the maximum possible loan (older borrowers may have to make bigger down payments).

For upgraders, a crucial hurdle is having sufficient funds to cover this down payment, after discharging the remaining flat loan and refunding used CPF monies.

But as the price gap between private homes and HDB flats widens, it becomes increasingly difficult to bridge this gap. A higher cash outlay to upgrade also means opportunity cost, as it’s cash that can’t be invested elsewhere.

As such, some Singaporeans are trying to upgrade not despite the high home prices, but rather because of them.

2. Private property ownership is still seen as a safety net

One of the woes of single-digit millionaires is that despite being in a higher wealth bracket, you’re still far from total financial security; at least with the cost of living in Singapore.

As such, a common sentiment is that a private property provides a “final fallback” if all else goes wrong. If your business falters, your stock portfolio falls apart, or you have urgent financial needs later, you can at least sell your condo or landed home (which would likely have appreciated over the years).

If you were to sell even a two-bedder condo unit (around 700 sq. ft.) at today’s average (based on the numbers above), that’s still around $1.08 million; enough to buy a 4-room or 5-room flat and still have substantial cash left over.

But if all you have is just your HDB flat, there’s much less room to manoeuvre. You might, for instance, downgrade from a $500,000 4-room flat to a $300,000 3-room flat, and have only $200,000 after the transaction. This may not suffice to maintain your financial goals during an emergency.

3. Legacy planning issues

As far as leaving an inheritance goes, resale flats are much less appealing than private homes.

One reason is that most Singaporeans are unable to inherit an HDB flat.

No one can own two HDB flats at once; so if your children already have a flat, they will have to keep one and sell the other. If they already own a private property, then you need to check if the flat was bought before 30th august 2010.

For flats bought after this date, your children must choose between keeping the flat or their private property. This almost invariably results in the flat being sold.

Even for flats bought before the date, your children can only retain the flat if they move into it (they can use the private property as a rental asset or for other purposes). Again, not a move that most people favour, so the flat tends to get sold.

There’s no guarantee that the flat will sell for a good price, when the time comes.

Let’s consider the fact that Singapore is an ageing society. At some point, there’s a risk of the previous generation leaving behind scores of vacant flats, which can’t be inherited – and the high supply then will likely limit their value.

4. Cash-Out Refinancing options for private homes

This is an often-overlooked advantage of private property ownership, which makes it favourable to sophisticated investors.

Cash-Out Refinancing allows you to borrow against the value if your property, within limits (typically up to 75 per cent of the property value, minus any CPF monies used). You can do this even for a property that’s not yet fully paid-up (although you must use the same bank that holds your mortgage).

Consider, for instance, a property valued at $2 million. You could potentially take a Cash-Out loan for up to $1.5 million against the property. The interest rate varies between banks as always; but because the Cash-Out loan is a form of secured lending, it tends to be cheaper than unsecured options such as personal loans or business loans.

Of course, you don’t need to take out the full loan amount. So you could, for instance, borrow just 50 per cent of the value ($1 million), as a potentially cheaper alternative to an unsecured line of credit.

As an aside, this also means you can get cash out of your private property without having to sell it or rent it out. This bypasses one of the main drawbacks of property assets, which is illiquidity.

Cash-Out Refinancing can only be done for private homes, never for HDB properties.

This isn’t to say every single-digit millionaire should rush out and upgrade. Our intent is just to provide some of the reasons why many continue to do so, even in a high-priced market. Do consult with a financial expert you trust, and remember to keep your portfolio diversified (don’t sink it all into one property!)

For more on related issues, do follow us on Single Digit Millionaire, as we look at the trends and struggles of the new middle-class.